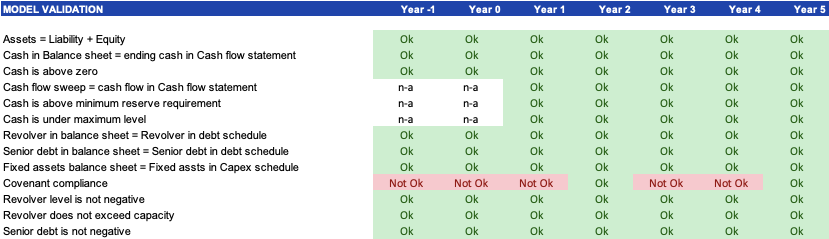

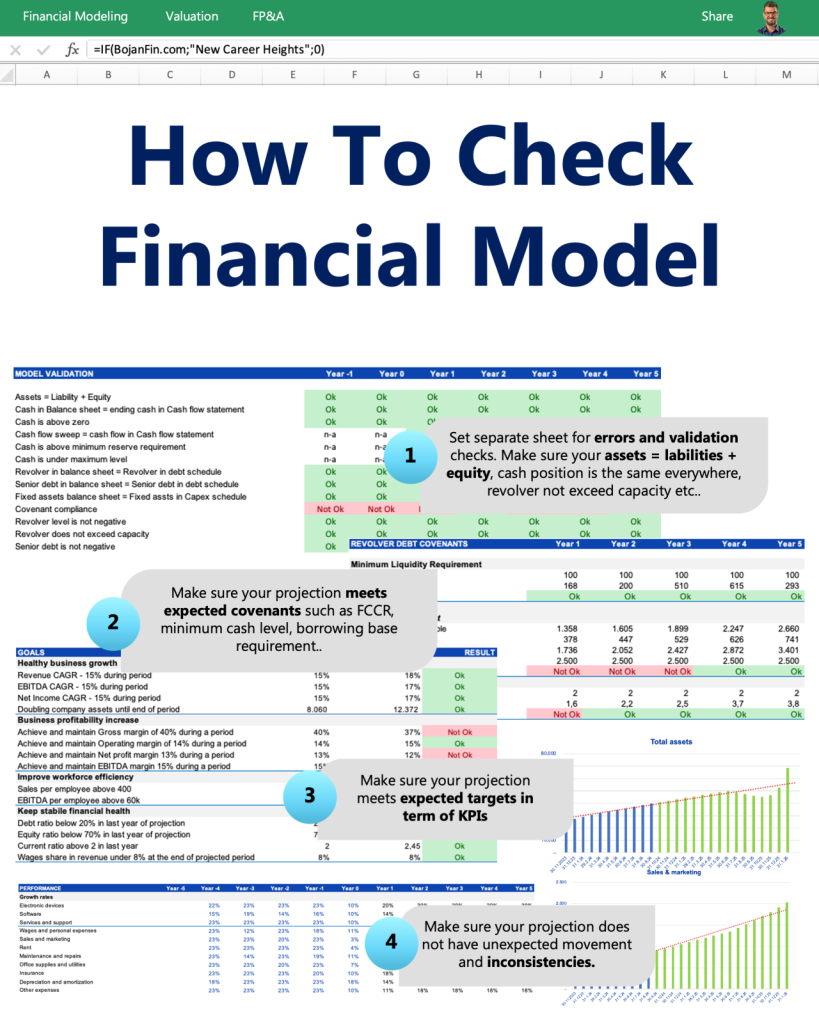

How to Check Your Financial Model

Your model will not be accurate if:

- Your assets are not equal to liabilities and equity.

- Ending cash in the balance sheet does not match the cash flow statement.

- Your projected revolver exceeds its capacity.

- Your cash balance shows a negative value.

Your model will not be effective if your projections look inconsistent and “weird.”

- Your projected performance is not in line with targeted KPIs.

- The outcomes do not match the expected covenants.

That’s why in every model, I prefer to set up different levels of checks and validation, including:

✔ Error checks

✔ Goal checks

✔ Consistency checks

✔ Covenant checks

✔ Cash requirement checks

I love using conditional formatting and setting up separate validation tables to visually track where I’m doing well and where improvements are needed.

How about you?

If you want to master the best financial modeling practices, click here join my FINANCIAL MODELING PROGRAM.

And one simple tip to wrap up:

In every sheet, freeze panes in the header and add a check to see if your balance sheet ties up.

You’ve probably experienced moving between sheets, and when you return to your projections, you spot an error—but you have no idea when you made the mistake. Then, you have to click undo sooooo many times.

Here is my visual for today. You can download it here.

How To Model LBO (Leveraged Buyout)

Have you ever tried to analyze acquisition effects in PE? This is a simple guide to begin.

🔹 What is an LBO?

LBO is the acquisition of a company using a significant amount of debt, with the company’s own cash flows used to pay down the debt over time. The goal is to maximize returns by using leverage while improving operational efficiency.

Basic information on our Paper LBO Model in this example

1) You are acquiring a company through LBO. Prior to acquisition, company was debt-free. Debt you issued to finance the acquisition will be repaid by Free Cash Flow company will generate

2) You plan to sell a company after 5 years

3) All Free Cash Flow Company generated during the 5 year period will be used for repayment of debt. Excess cash after paying debt will increase Equity value.

🔹 Step 1: Define the Key Assumptions

Before building the model, you need to define the inputs and assumptions that will drive the calculations.

📌 Key LBO Model Assumptions

- Entry Enterprise Value → The price paid for the company.

- Debt Financing → The amount and types of debt used (e.g., senior debt, mezzanine).

- Equity Contribution → The portion of the purchase price funded by investors.

- Revenue Growth & Margins → Expected financial performance.

- Debt Paydown Schedule → How much debt will be repaid yearly.

- Exit Multiple & Timing → Expected valuation at the time of sale (typically 5 years).

🔹 Step 2: Build the Financial Statements

An LBO model relies on three key statements:

✔️ Income Statement → Shows revenue, profitability, and EBITDA.

✔️ Cash Flow Statement → Determines how much Free Cash Flow (FCF) is available for debt repayment.

✔️ Balance Sheet → Tracks debt reduction and equity growth.

📌 2.1 Build the Income Statement

- Start with Revenue Projections (use historical growth trends or industry estimates).

- Deduct COGS and Operating Expenses to get EBITDA.

- Subtract Depreciation & Amortization (D&A) to get EBIT (Operating Profit).

- Deduct Interest Expense (from debt financing).

- Apply Taxes to arrive at Net Income.

✅ Key Formula:

EBITDA=Revenue−COGS−Operating Expenses

📌 2.2 Build the Cash Flow Statement

The Cash Flow Statement determines how much Free Cash Flow (FCF) is available to pay off debt.

- Start with Net Income.

- Add back Non-Cash Expenses (Depreciation & Amortization).

- Adjust for Changes in Working Capital.

- Deduct Capital Expenditures (CapEx).

- The result is FCF, which will be used to pay off debt.

✅ Formula:

FCF=EBITDA−CapEx−Taxes−Changes in Working Capital

📌 2.3 Model Debt Repayment

- Determine the beginning debt balance.

- Subtract annual debt repayments (use all available FCF for debt reduction).

- Calculate new interest expense based on remaining debt.

- Repeat until debt is fully repaid (usually by Year 5).

✅ Formula for New Debt Balance:

Debt Balance (Year X)=Debt Balance (Year X-1)−Annual Repayment

🔹 Step 3: Calculate Exit Value and Investor Returns

At the end of the LBO period (e.g., 5 years), the company is sold at an assumed EBITDA multiple.

📌 3.1 Calculate Exit Enterprise Value

- Multiply Final Year EBITDA by the Exit Multiple.

✅ Formula:

Exit Value=Final Year EBITDA×Exit Multiple

- Subtract remaining debt to get Equity Value at Exit.

✅ Formula:

Equity Value=Exit Enterprise Value−Remaining Debt

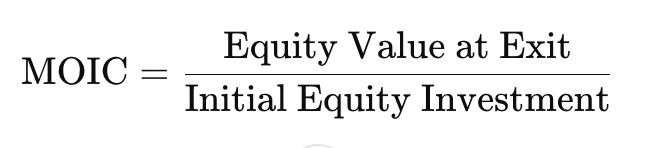

📌 3.2 Calculate Investor Returns

Investor returns in an LBO are measured using IRR (Internal Rate of Return) and MOIC (Multiple on Invested Capital).

✅ Formula for IRR:

(where n = number of years in the investment period)

✅ Formula for MOIC:

🎯 Target IRR: Private equity firms typically aim for 20-30% IRR.

🔹 Step 4: Sensitivity Analysis

To test different outcomes, conduct a sensitivity analysis by adjusting:

- Revenue Growth

- EBITDA Margins

- Exit Multiple

- Leverage Ratio (Debt %)

✅ Example: What happens if EBITDA grows faster or the exit multiple is lower? ✔️ Use Excel Data Tables to create multiple outcome scenarios.

🔹 Summary: Full LBO Model Steps

1️⃣ Define Key Assumptions (Purchase Price, Debt %, Revenue Growth).

2️⃣ Build the Income Statement (EBITDA, Interest Expense, Net Income).

3️⃣ Calculate Free Cash Flow (FCF) (for debt repayment).

4️⃣ Model Debt Repayment (track remaining balance).

5️⃣ Estimate Exit Value & Equity Growth.

6️⃣ Calculate IRR and MOIC (Investor Returns).

7️⃣ Perform Sensitivity Analysis.

LBO template is included as additional resource of FINANCIAL MODELING PROGRAM.

Want this visual? Download here.