2 Excel templates:

1) Matching Trial Balance and CoA

The CoA sheet contains the chart of accounts with mapping.

Columns:

𝗖𝗵𝗮𝗿𝘁 𝗼𝗳 𝗔𝗰𝗰𝗼𝘂𝗻𝘁𝘀 – The list of GL accounts

𝗚𝗿𝗼𝘂𝗽 – most important because it is used in all subsequent sheets, and reports

𝗗𝗲𝗯𝗶𝘁/𝗖𝗿𝗲𝗱𝗶𝘁 – Indicates whether the account is debited or credited

𝗣𝗼𝘀𝗶𝘁𝗶𝗼𝗻 – Specifies the financial statement position it belongs to.

The key here is to have more automated reporting.

The idea here is :

👉 Input your trial balance in Data input sheet

👉 Insert groups by =VLOOKUP formula

👉 SUM groups into financial statements

I’ve pasted data here as examples for all months starting from January 31, 2024, to December 31, 2024.

Click here to get your Excel template

The model can be adjusted very easily to any company. This template is resulted by a full reporting package, forecasting files and schedules. I do not share such templates this time, I focus just on the importance of presentation.

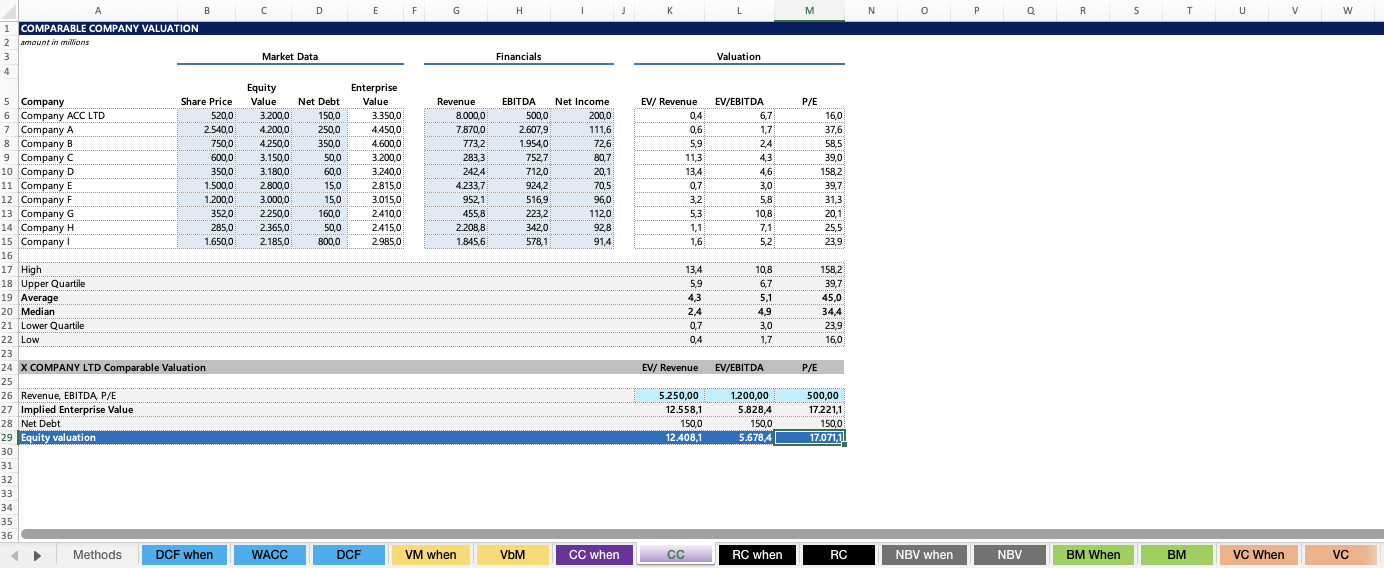

2) Startup Valuation Models

7 methods included with the explanation of when the method is appropriate to use and valuation calculation under given assumptions:

Discounted cash flow method

Valuation by multiple (EBITDA or Revenue/ARR)

Comparable companies method

Replacement cost method

Net book value method

Berkus method

Venture capital method

Click here to get your Excel template

This model, with small adjustments can be used for many industries.

Here are 2 Infographics for Today:

1) Finance Model Design

Get this infographic on a high-resolution PDF

2) How to Maximize the Value of Your Company

Get this infographic on a high-resolution PDF

Here’s today’s “How to” guide:

Step-by-Step Guide to Applying EBITDA Multiple Valuation

1. Determine EBITDA as it is

- EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. It is a measure of a company’s operating performance and profitability.

Example:

- Revenue: $10 million

- COGS: $5 million

- SG&A: $1 million

- Depreciation: $0.5 million

- Interest: $0.2 million

- Taxes: $0.3 million

EBITDA = Revenue – COGS – SG&A = $10 million – $5 million – $1 million = $4 million

2. Make EBITDA Adjustments

EBITDA may need adjustments to reflect the true operating performance of the business, especially in private equity deals. The adjustments can be one-time, non-recurring expenses or revenue items.

- One-time expenses: These are expenses that won’t recur in the future (e.g., legal fees, restructuring costs).

- Owner compensation: If the business is owner-operated, the salary taken by the owner may not reflect the market rate for someone in that position.

- Non-core operations: Revenue or expenses related to activities not part of the core operations should be adjusted.

Example:

- EBITDA (before adjustments): $4 million

- Adjustment for non-recurring legal fees: $0.1 million

- Adjustment for owner’s compensation (over market rate): $0.2 million

Adjusted EBITDA = $4 million + $0.1 million + $0.2 million = $4.3 million

3. Apply EBITDA Multiple

Once you have the adjusted EBITDA, apply an industry-specific multiple to determine the enterprise value (EV). The multiple is often based on comparable companies or precedent transactions in the industry.

Example:

- EBITDA Multiple: 6x

- Adjusted EBITDA: $4.3 million

Enterprise Value = 6 × $4.3 million = $25.8 million

4. Adjust for Net Debt

To arrive at the equity value, subtract the company’s net debt from the enterprise value.

Example:

- Enterprise Value: $25.8 million

- Debt: $5 million

- Cash: $2 million

Net Debt = Debt – Cash = $5 million – $2 million = $3 million

Equity Value = Enterprise Value – Net Debt = $25.8 million – $3 million = $22.8 million

5. Adjust for Working Capital

If net working capital (NWC) differs from a normalized level (target NWC), an adjustment will be made to equity value. Working capital adjustments ensure the business has sufficient cash to operate post-transaction.

Example:

- Target NWC: $1 million

- Actual NWC: $0.8 million

NWC Adjustment = $1 million – $0.8 million = $0.2 million

Adjusted Equity Value = $22.8 million – $0.2 million = $22.6 million

6. Consider Other Adjustments

Adjustments might also be made for items like:

- Deferred revenue

- Accrued expenses

- Off-balance sheet liabilities

Step-by-Step for Transaction Structuring with Contingent Payments

In many private equity transactions, a portion of the purchase price is contingent on future performance. Let’s assume the transaction is structured so that 50% of the price is paid upfront, and 50% is contingent on hitting future EBITDA targets after one year.

1. Initial Purchase Price

The initial purchase price is typically based on the current valuation.

Example:

- Adjusted Equity Value: $22.6 million

- 50% upfront payment: $11.3 million

2. Structure Contingent Payments

The contingent payment will be based on future performance metrics, such as the EBITDA achieved after one year.

Example Structure:

- The remaining 50% ($11.3 million) will be paid if the company achieves an EBITDA of $5 million in year one.

- If EBITDA is less than $5 million, the contingent payment will be reduced on a sliding scale.

Contingency Formula:

- If EBITDA is $4 million (below target), then the payment might be adjusted proportionally. For example, if the EBITDA is only 80% of the target, then the contingent payment will be 80% of the remaining $11.3 million.

Adjusted Payment = Contingent Payment × (Actual EBITDA / Target EBITDA) = $11.3 million × (4 million / 5 million) = $9.04 million

3. Earn-Out Agreement

This earn-out can be structured with a time frame (e.g., one year), and clearly defined targets. The buyer and seller agree on terms such as:

- Time frame for achieving targets (one year).

- Metrics used (EBITDA, revenue, etc.).

- Calculation method for the contingent portion.

4. Adjust for Other Contingencies

The agreement may also include:

- Performance clauses for revenue, working capital, or customer retention.

- Protections for both parties, such as setting a minimum contingent payment.

Example Summary

- Upfront Payment: $11.3 million paid at closing.

- Earn-Out: Up to $11.3 million contingent on achieving $5 million EBITDA within one year.

- If the EBITDA is $4 million (80% of the target), the earn-out payment would be $9.04 million.

Final Considerations

- Due Diligence: Ensure thorough due diligence on working capital, debt levels, and normalization adjustments.

- Sensitivity Analysis: Analyze different scenarios for future performance to understand the range of potential outcomes for contingent payments.

- Negotiation: Structure the deal terms to ensure alignment between buyer and seller for long-term success.